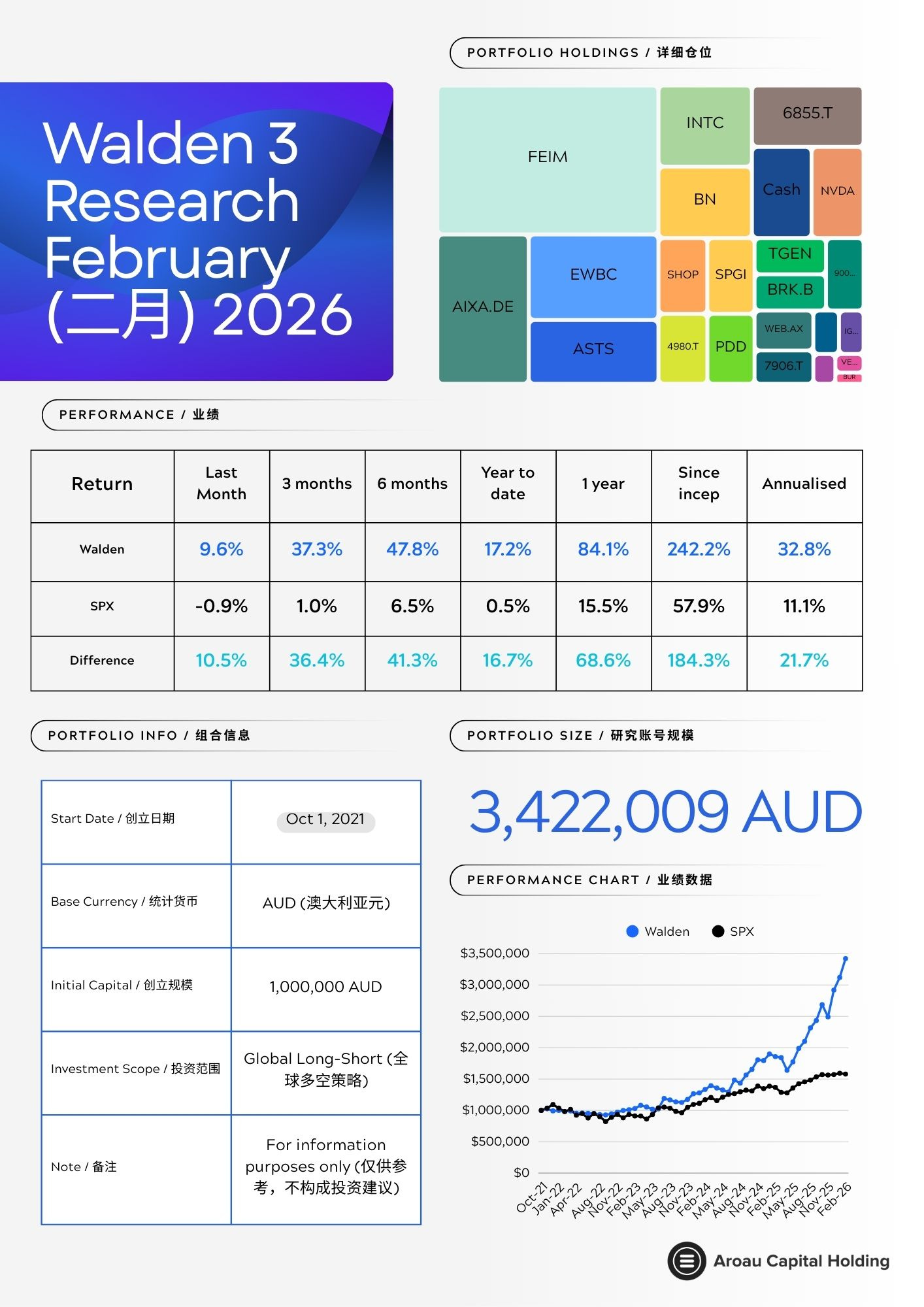

February Portfolio

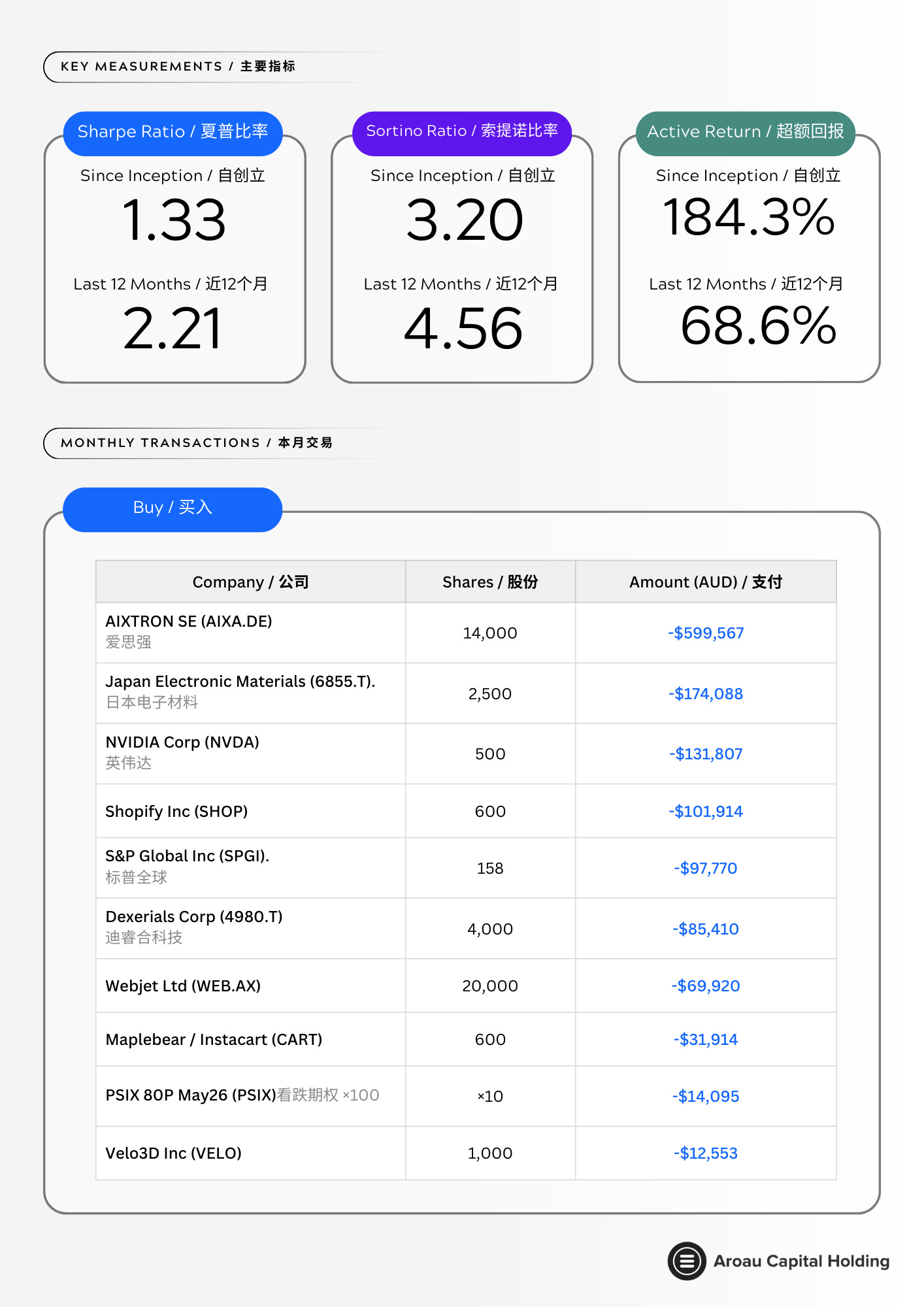

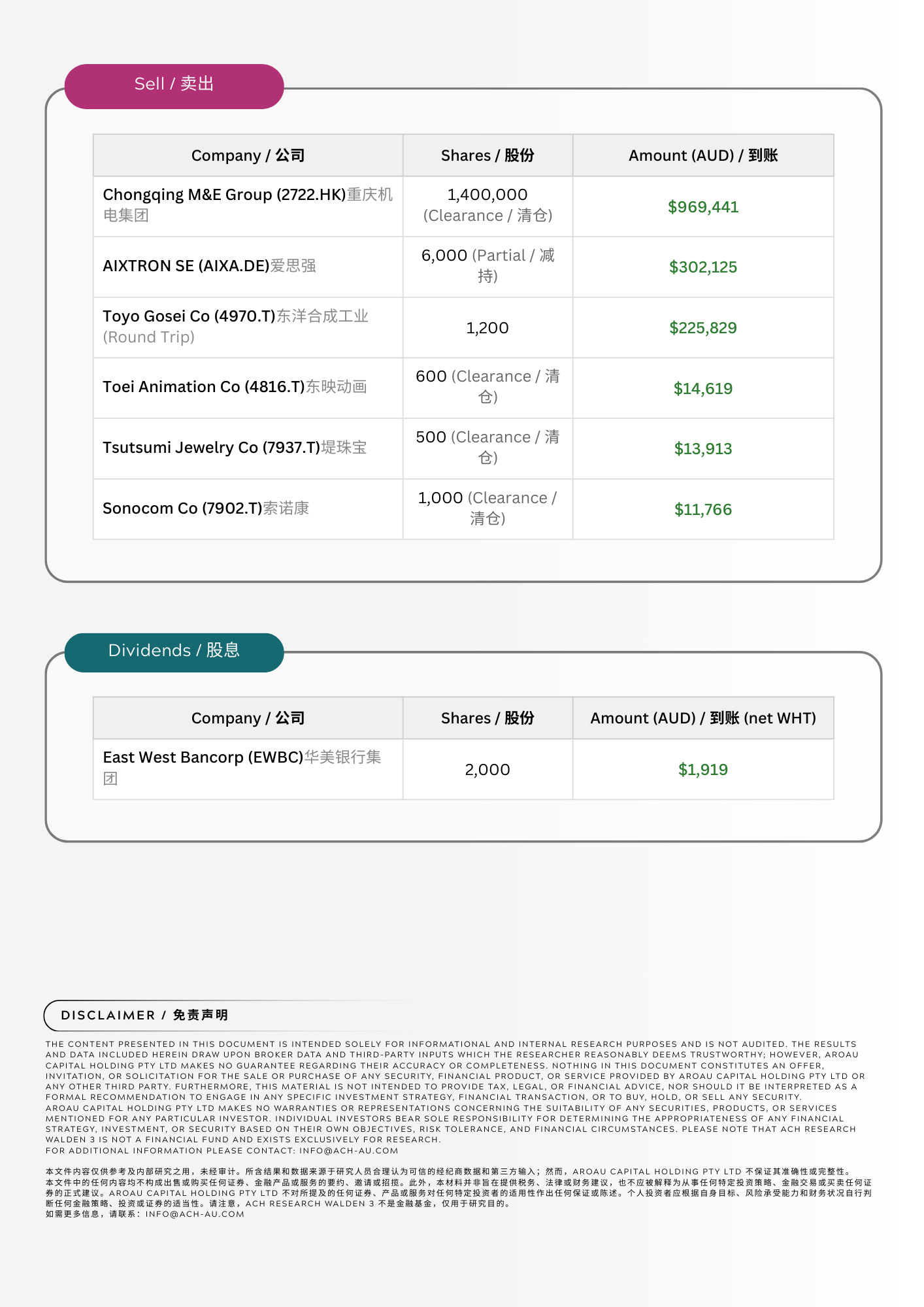

Buy AIXA.DE, 6855.T Sell 2722.HK, 4816.T, 7937.T, 7902.T

Manager’s Commentary

February was an active month for the portfolio. The S&P 500 fell 0.9%, masking historic sector turbulence underneath a flat headline number. A violent rotation out of SaaS and software stocks into value and commodity names dominated the first three weeks, before U.S. and Israeli military strikes on Iran (“Operation Epic Fury”) added a geopolitical shock in the final days of the month. Walden 3 returned +9.6% for February.

Exits and Trimming

The largest single action was the full exit of Chongqing M&E (2722.HK), clearing 1.4 million shares. The stock had appreciated roughly 260% from the original entry and, by late February, traded at the manager’s bullish case price target of approximately HK$3.40. At that level the probability weighted expected return no longer justified the position size. H1 2025 net income was up 155% and the stock exceeded the sole analyst price target of HK$3.04, confirming thin coverage and limited institutional interest as structural features of the opportunity rather than flaws. A partial sale of AIXTRON (6,000 of 14,000 shares, AUD 302,125) locked in gains while retaining exposure to the CPO thesis at a reduced cost basis. Four small Japanese positions (Toei Animation, Tsutsumi Jewelry, Sonocom) were cleared, alongside a round trip in Toyo Gosei (4970.T) that captured approximately 38% return on a short duration trade.

New Positions

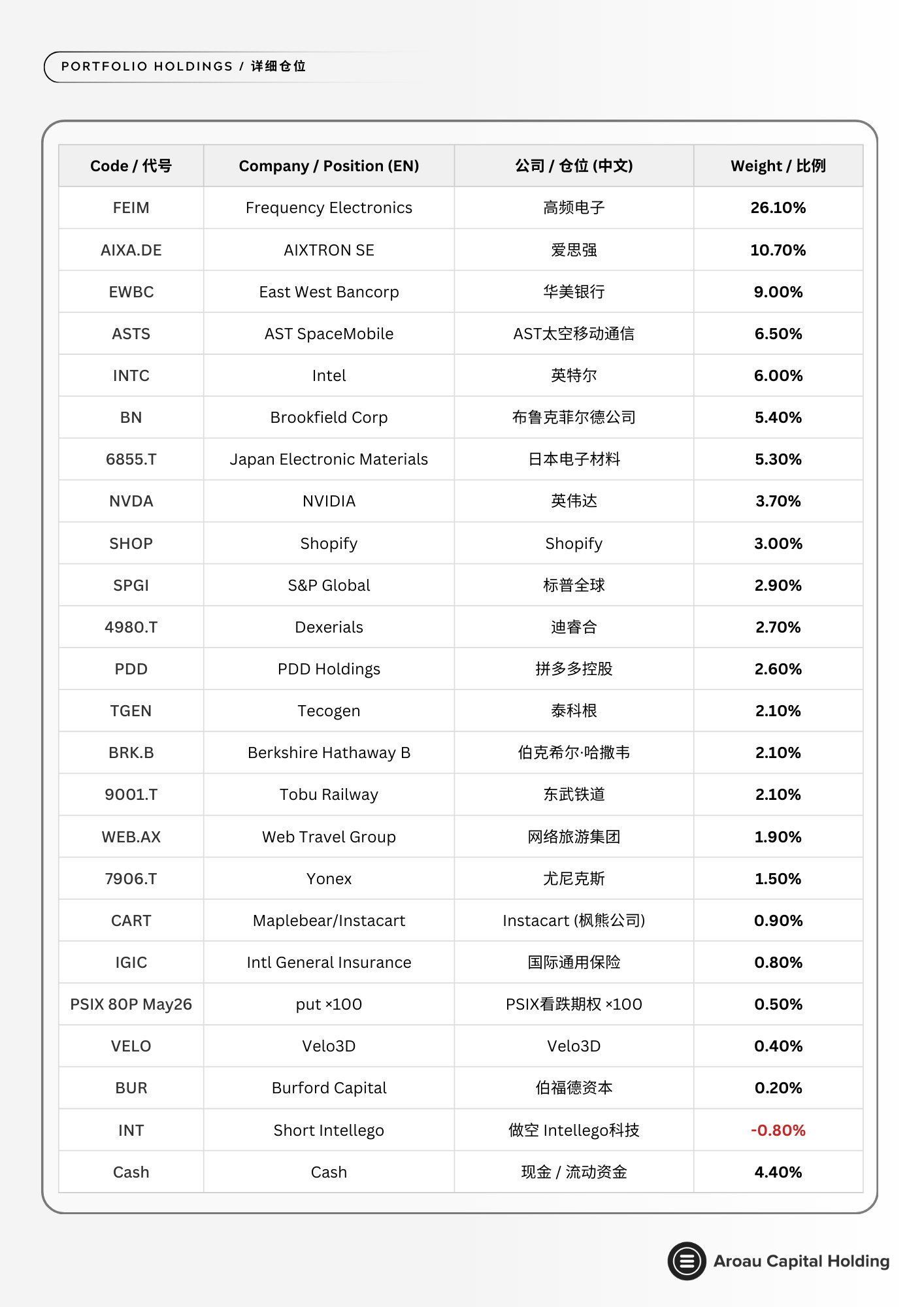

The February buying programme centred on two themes: (1) AI physical layer infrastructure, and (2) the SaaS selloff creating mispricing in non SaaS businesses swept up in indiscriminate selling.

NVIDIA (NVDA) was added as a direct expression of the AI infrastructure buildout. NVIDIA reported Q4 FY2026 on 25 February: record quarterly revenue of $68.1 billion (+73% year on year), with data centre revenue alone at $62.3 billion (+75%). Full year FY2026 revenue was $215.9 billion (+65%). Non GAAP gross margin held at 75.2%. Q1 FY2027 guidance of $78 billion (plus or minus 2%) exceeded the $72.6 billion consensus by a wide margin, and notably assumes zero data centre compute revenue from China. Jensen Huang described the “agentic AI inflection point” as arrived, with combined hyperscaler capex approaching $700 billion annually. The stock sold off 5.5% on the report despite beating on all metrics, reflecting a market that has priced in perfection and now requires a clear 2027 growth path. The manager views the selloff as a reasonable entry point for a small position in the highest quality name in the AI infrastructure chain, with the Vera Rubin platform (first samples shipped to customers in late February) providing the next product cycle catalyst.

Dexerials (4980.T) offers a dual catalyst: near term iPhone Fold content uplift and medium term CPO photonics. Dexerials holds 74% global share in anisotropic conductive film (ACF) and 94% in anti reflection film, both critical for foldable OLED assembly. Apple’s iPhone Fold, expected in autumn 2026 with a book style design and near crease free display, would meaningfully increase Dexerials’ content per device versus a standard iPhone (two display panels, flexible interconnects, additional OCA bonding). Separately, Dexerials launched its Photonics Solutions subsidiary in April 2024, developing waveguide photodiodes already exceeding 60 GHz bandwidth, with a 400 Gbps/lane CPO targeted roadmap by 2030.

Shopify (SHOP) was swept up in the “SaaSpocalypse” that wiped over $1 trillion from software market capitalisation in early February, triggered by AI agent launches from Anthropic and others. The manager believes Stratechery’s analysis provided the clearest framework: unlike per seat SaaS businesses threatened by AI automation, Shopify is fundamentally a commerce infrastructure and payments platform. In 2025, merchant solutions (payments, capital, POS) generated $8.8 billion versus only $2.75 billion in subscriptions. That means 76% of revenue is commission based on GMV, not headcount. AI driven shopping orders through ChatGPT, Gemini, and Copilot grew 15x over 2025, with Shopify powering the checkout behind them. Shopify is an AI beneficiary masquerading as a SaaS victim.

Maplebear/Instacart (CART) offers an unusual governance angle: former CEO Fidji Simo departed in August 2025 to become OpenAI’s first CEO of Applications (aka Ads), reporting directly to Sam Altman, while remaining Chair of Instacart’s board. This dual positioning gives CART unusual proximity to frontier AI product development. The stock was purchased on a clean Q4 2025 print showing 12% revenue growth and $303 million adjusted EBITDA. S&P Global (SPGI) reflects a similar logic: financial data infrastructure with deep moats mistakenly sold alongside commoditised SaaS names.

Webjet (WEB.AX) was initiated after the stock lost 37% in a single session following disclosure of a Spanish tax audit at its “Mundo” subsidiary in the Balearic Islands, covering 2021 to 2025. The reaction appears disproportionate: the audit is at its earliest stage (a questionnaire), the subsidiary in question is only one of two Spanish entities, and management reiterated full year guidance of AUD 147 to 155 million EBITDA with approximately AUD 450 million in cash. For every AUD 100 million net tax liability, fair value declines only about 5% or AUD 0.30 per share. Two prior confidence eroding events (WebBeds margin compression in October 2024 and a minor accounting restatement in November 2024) appear to have primed the market for an outsized response to any negative headline, creating asymmetric value.

Position Reviews

Frequency Electronics (FEIM). Valuation rests on FEIM’s position as the premier supplier of precision timing and frequency control products (atomic clocks, rubidium oscillators, GPS disciplined oscillators) to U.S. aerospace and defence customers, backed by a record $71 million backlog and a new quantum sensing facility in Boulder, Colorado staffed by senior scientists recruited from NIST’s Time and Frequency Division. Q3 FY2026 guidance calls for 8 to 10% revenue growth and adjusted EPS of $0.19 to $0.21. The manager views FEIM as a scarce, vertically integrated defence timing franchise with quantum sensing optionality, and the position size reflects high conviction in multiyear revenue compounding as defence modernisation programmes accelerate.

AIXTRON SE (AIXA.DE). Initiated and partially trimmed during the month (net 8,000 shares retained). AIXTRON holds a near monopoly (>90% share) in the MOCVD epitaxy tools used to produce indium phosphide wafers, the critical compound semiconductor substrate for external laser sources in co packaged optics (CPO). As AI data centre bandwidth demands push from pluggable transceivers toward CPO architectures, every major InP fab (Coherent, Lumentum, SMART Photonics, IQE) depends on AIXTRON’s G10 AsP platform. Nokia’s purchase of the G10 AsP in April 2025, shortly after Nvidia’s $1 billion investment in Nokia, confirmed the supply chain linkage. Management expects optoelectronics revenue to more than double year on year from 2025 into 2026. The partial sale early in the month was tactical, locking in gains on the first tranche while maintaining core exposure.

East West Bancorp (EWBC). EWBC reported Q4 2025 on 22 January: record full year net income of $1.3 billion, EPS of $9.52, return on tangible common equity of 17%, and a 33% dividend increase to $0.80 per quarter. Q4 revenue was $758 million, beating consensus. Full year 2025 saw records across revenue, net interest income, fee income (+12% year on year, with wealth management fees up 29%), EPS, loans, and deposits. Asset quality remains excellent with full year net charge offs of just 11 basis points and Q4 net charge offs of 8 basis points. CET1 capital stands at 15.1%. For 2026, management guided 5 to 7% loan growth (led by C&I and residential mortgages), 5 to 7% NII growth, and operating expenses up 7 to 9% as the bank invests in technology and headcount. The efficiency ratio was 34.5% in Q4, among the best in the industry.

AST SpaceMobile (ASTS). ASTS reported Q4 2025 on 2 March (after month end): full year 2025 revenue of $70.9 million in its first year as a revenue generating business, Q4 revenue of $54.3 million (beating consensus by 38%), and over $1.2 billion in contracted revenue commitments from MNO partners. The company successfully deployed BlueBird 6, the largest commercial communications array ever placed in low Earth orbit, which is expected to exceed 120 Mbps peak speeds. BlueBird 7 was encapsulated at Cape Canaveral in February with launch expected in March. Management targets 45 to 60 satellites in orbit by year end 2026, with launches every one to two months. Pro forma liquidity stands at $3.9 billion following the convertible notes offering. The 2026 revenue guide of $150 to $200 million reflects pre commercial service ramp, with the $1 billion 2027 target supported by roughly half the pipeline already booked or contracted. Key milestones ahead: stacked launches (groups of 3, 4, 6, or 8 satellites) beginning after BB7, and integration of a custom ASIC chip targeting 10 GHz processing bandwidth per satellite. The thesis remains high conviction, high risk: a first mover in direct to device cellular broadband with irreplaceable spectrum and partnership assets, but execution on manufacturing cadence and commercial activation is the gating factor.

Intel (INTC). Initiated in January, no activity in February. The thesis centres on CEO Lip Bu Tan’s track record at Cadence and the structural case for x86 infrastructure in the AGI buildout. Intel remains the only Western manufacturer with leading edge foundry capability (alongside TSMC), and the geopolitical imperative to maintain domestic semiconductor manufacturing capacity provides a floor under the restructuring story. The position was initiated at a low multiple to tangible book and is sized for a multiyear turnaround with significant optionality on foundry services and government subsidies. NVIDIA’s Q4 FY2026 results (reported 25 February) reinforce the broader demand environment: $68.1 billion in quarterly revenue (+73% year on year), $62.3 billion from data centre alone (+75%), and Q1 FY2027 guidance of $78 billion. Combined hyperscaler capex is approaching $700 billion annually. This demand backdrop validates the structural need for diversified semiconductor manufacturing capacity, which is the core of the Intel position.

Brookfield Corporation (BN). Brookfield continues to compound across its infrastructure, renewable power, private equity, and real estate platforms. The position reflects the manager’s view that BN is a best in class alternative asset manager trading at a meaningful discount to intrinsic value when the embedded carried interest and fee related earnings in its $1 trillion+ AUM base are properly valued. The Iran strikes and resulting energy price volatility (Brent crude hitting a 52 week high above $78, Maersk suspending Strait of Hormuz transits) are a net positive for Brookfield’s infrastructure and energy transition platforms, which benefit from elevated commodity prices and increased urgency around energy security investment.

Japan Electronic Materials (6855.T). Initiated during the month (2,500 shares). JEM is a memory focused pure play probe card manufacturer whose economics improve dramatically with HBM: standard DRAM probe cards sell for $30,000 to $50,000 while HBM probe cards command $100,000 to $200,000+, a 3 to 4x ASP uplift driven by pin counts exceeding 150,000 per die. HBM4, ramping through 2026 at SK Hynix and Samsung, doubles I/O to 2,048 terminals and introduces logic base dies for the first time, further increasing test complexity and needle wear. JEM reported 70% revenue growth and 3x operating profit growth in its most recent quarter. The stock has run up significantly (+422% five years) yet still trades at roughly 12.8x trailing earnings with ¥15.4 billion net cash. The “Known Good Die” imperative (stress testing every layer before stacking to avoid scrapping entire HBM assemblies) ensures high recurring demand as HBM volumes scale.